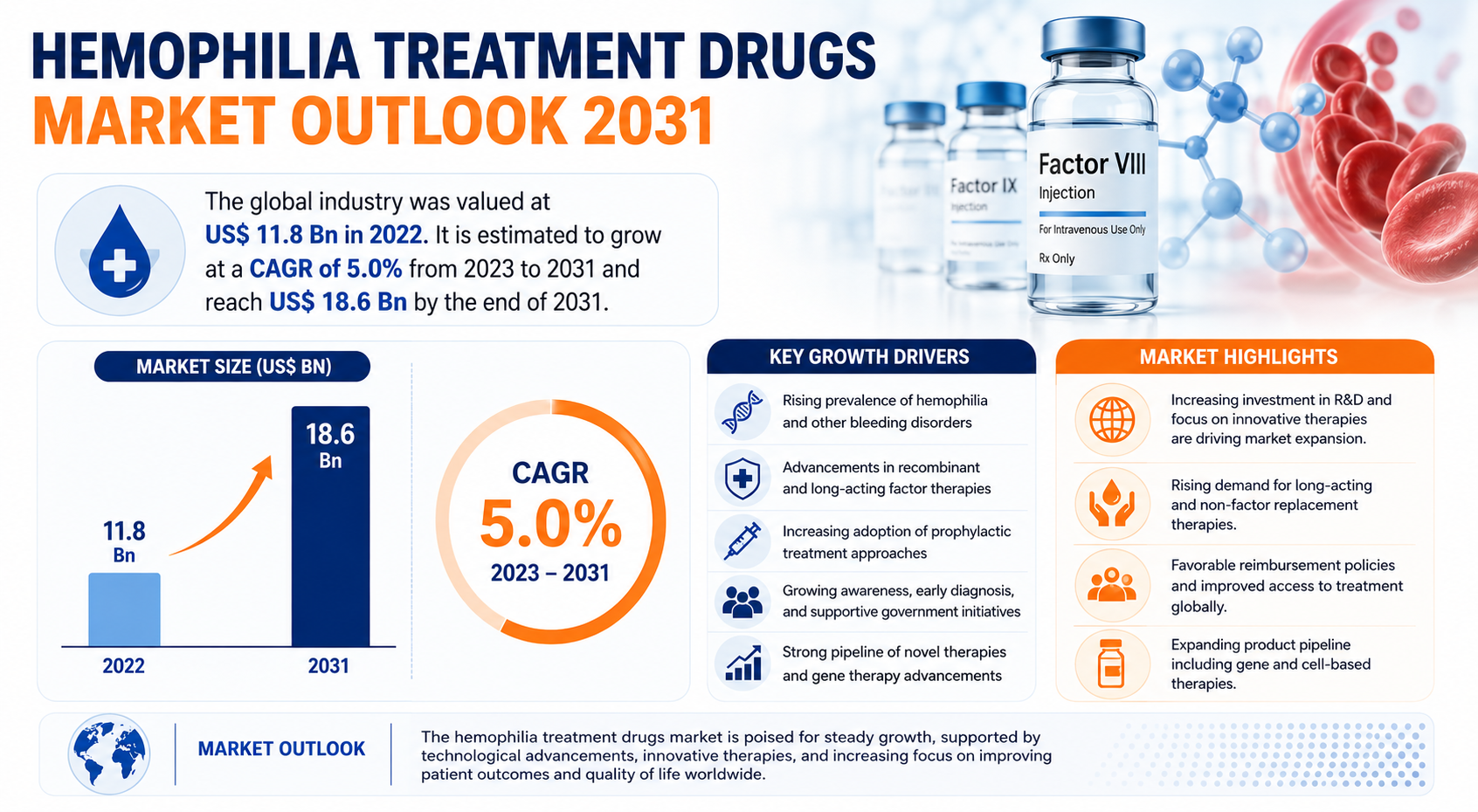

The global hemophilia treatment drugs market is witnessing substantial growth due to rapid advancements in biotechnology, increasing prevalence of hemophilia, and the development of innovative treatment approaches. According to recent industry analysis, the global hemophilia treatment drugs market was valued at US$ 11.8 billion in 2022 and is projected to reach US$ 18.6 billion by 2031, expanding at a CAGR of 5.0% during the forecast period from 2023 to 2031.

The market is undergoing a transformative shift from conventional plasma-derived therapies toward recombinant coagulation factor concentrates, RNA-based therapies, and non-factor replacement therapies. Pharmaceutical companies are aggressively investing in research and development to launch safer, long-acting, and more effective therapies that improve patient outcomes and reduce treatment frequency.

Explore pivotal insights and conclusions from our Report in this sample –

https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=1900

Market Overview

Hemophilia is a rare inherited bleeding disorder in which the blood fails to clot properly due to deficiency or absence of clotting factors. The disease primarily affects males and is categorized mainly into hemophilia A and hemophilia B. Patients suffering from hemophilia experience prolonged bleeding episodes, spontaneous internal bleeding, and joint damage if left untreated.

The increasing incidence of hemophilia across developed and developing nations is creating strong demand for advanced treatment drugs. According to the Centers for Disease Control and Prevention (CDC), approximately 400 babies are born with hemophilia A every year in the United States, while nearly 33,000 men in the country are affected by the disorder.

The market has evolved significantly with the emergence of recombinant coagulation factor concentrates and novel non-replacement therapies. These therapies are offering enhanced efficacy, fewer side effects, and improved patient convenience compared to traditional plasma-derived products.

In addition, rising awareness programs, government support for rare disease treatment, and increasing access to healthcare infrastructure are supporting market growth globally.

Key Market Growth Drivers

Rising Research & Development Activities

Research and development activities remain one of the strongest growth pillars for the hemophilia treatment drugs market. Leading pharmaceutical and biotechnology companies are investing heavily in innovative therapies designed to improve hemostatic balance and minimize bleeding episodes.

Novel treatment approaches such as Anti-TFPI therapies are gaining traction due to their ability to reduce bleeding by slowing the anticoagulation mechanism. Unlike conventional therapies that replace missing clotting factors, Anti-TFPI therapies restore hemostatic balance by targeting tissue factor pathway inhibitor mechanisms.

Similarly, RNA interference (RNAi)-based therapies are revolutionizing hemophilia treatment by targeting antithrombin production. These therapies help restore sufficient thrombin generation, thereby reducing bleeding episodes in both hemophilia A and hemophilia B patients.

Growing Demand for Long-acting Non-replacement Therapies

Long-acting non-replacement therapies are becoming increasingly popular because they reduce dosing frequency and improve patient adherence. Fitusiran, an investigational small interfering RNA (siRNA) therapy, is currently being studied as a prophylactic treatment administered monthly or every other month.

The growing preference for subcutaneous administration over intravenous infusion is another major factor boosting adoption of these therapies. Patients and healthcare providers are increasingly favoring treatments that improve convenience and quality of life.

Increasing Prevalence of Hemophilia

The growing number of diagnosed hemophilia cases worldwide is positively impacting market demand. Enhanced diagnostic capabilities and improved disease awareness are enabling earlier diagnosis and treatment initiation.

Moreover, advancements in genetic testing technologies are helping identify hemophilia cases more efficiently, especially in emerging economies.

Government Support and Funding

Government agencies and healthcare organizations across various countries are funding research activities related to hemophilia treatment. Public funding for hemophilia treatment centers and rare disease programs is contributing significantly to market expansion.

In the United States, more than 100 federally funded Hemophilia Treatment Centers (HTCs) provide comprehensive treatment, education, and support services to patients.

Analysis of Key Players – Key Player Strategies

The competitive landscape of the hemophilia treatment drugs market is characterized by strong investment in innovation, strategic collaborations, mergers & acquisitions, and product launches.

Major market participants include:

- Pfizer Inc.

- CSL Behring

- Kedrion

- Takeda Pharmaceutical Company Limited

- Novo Nordisk A/S

- Bayer AG

- F. Hoffmann-La Roche Ltd.

- Octapharma AG

- Biotest AG

- Sanofi S.A.

Innovation-focused Strategies

Leading companies are focusing on expanding their recombinant therapy portfolios and accelerating clinical trials for gene-based and RNA-based therapies. Companies are prioritizing the development of therapies with improved efficacy, longer half-life, and lower administration frequency.

Strategic Collaborations and Partnerships

Market participants are entering into partnerships with biotechnology firms and research institutions to accelerate innovation and commercialization. These collaborations are helping companies strengthen product pipelines and improve market positioning.

Geographic Expansion

Major pharmaceutical companies are expanding their footprint in emerging markets such as India, China, Brazil, and ASEAN countries where diagnosis rates and treatment accessibility are improving steadily.

Mergers and Acquisitions

Acquisitions of smaller biotech firms with promising clinical pipelines are helping established companies diversify their product offerings and strengthen competitive advantage.

Market Challenges & Opportunities

Challenges

High Treatment Costs

Hemophilia therapies, especially recombinant factors and gene therapies, are extremely expensive. The high cost of lifelong treatment creates affordability challenges, particularly in low- and middle-income countries.

Limited Access in Developing Regions

Despite growing awareness, several regions still lack adequate diagnostic facilities and treatment infrastructure. Many patients remain undiagnosed or untreated due to poor healthcare accessibility.

Risk of Inhibitor Development

Some patients develop inhibitors that reduce the effectiveness of factor replacement therapies. Managing inhibitor-related complications remains a major clinical challenge.

Regulatory Complexities

Stringent regulatory approval processes for biologics and gene therapies can delay product launches and increase development costs.

Opportunities

Emergence of Gene Therapy

Gene therapy represents one of the most promising opportunities in the market. Advanced therapies under clinical development have the potential to provide long-term or even curative outcomes for hemophilia patients.

Personalized Medicine

The shift toward personalized treatment approaches is opening new growth avenues for pharmaceutical companies. Tailored therapies based on patient genetics and disease severity are expected to improve treatment outcomes significantly.

Expansion in Emerging Markets

Countries in Asia Pacific and Latin America present strong growth potential due to rising healthcare expenditure, increasing awareness, and improved access to recombinant therapies.

Technological Advancements

Advancements in biotechnology, RNA interference technologies, and extended half-life therapies are expected to create substantial future growth opportunities.

Key Player Strategies

Key companies operating in the market are adopting several strategic initiatives to maintain competitive advantage:

- Expansion of recombinant coagulation factor portfolios

- Investment in RNA interference and gene therapy technologies

- Product approvals and commercialization strategies

- Partnerships with healthcare providers and research institutions

- Strengthening manufacturing capabilities

- Increasing penetration in emerging economies

- Focus on long-acting therapies with enhanced patient convenience

- Clinical trial expansion for innovative biologics

These strategies are helping companies enhance market share and improve long-term revenue growth.

Recent Developments

- In February 2023, The U.S. Food and Drug Administration (FDA) approved Sanofi’s ALTUVIIIO [Antihemophilic Factor (Recombinant), Fc-VWF-XTEN Fusion Protein-ehtl], previously referred to as efanesoctocog alfa, a first-in-class, high-sustained factor VIII replacement therapy. ALTUVIIIO is indicated for routine prophylaxis and on-demand treatment to control bleeding episodes, as well as perioperative management (surgery) for adults and children with hemophilia A.

- In February 2020, Novo Nordisk launched ESPEROCT, the company’s long-acting recombinant factor VIII product for the prevention and treatment of bleeding in individuals with hemophilia A.

Investment Landscape and ROI Outlook

The hemophilia treatment drugs market is attracting significant investments from pharmaceutical companies, venture capital firms, and government organizations due to the increasing commercial potential of advanced biologics and gene therapies.

Investments are primarily focused on:

- Recombinant factor development

- RNA-based therapeutics

- Gene therapy platforms

- Long-acting biologics

- Clinical trial expansion

- Manufacturing infrastructure

The market offers strong long-term return on investment (ROI) potential because hemophilia is a chronic condition requiring lifelong treatment. The increasing adoption of premium-priced therapies and rising patient diagnosis rates are expected to generate stable revenue streams for market participants.

Additionally, orphan drug incentives, regulatory exclusivity benefits, and premium reimbursement structures are making the market highly attractive for investors.

Biotechnology companies involved in innovative hemophilia therapies are expected to witness robust valuation growth during the forecast period.

Market Segmentations

By Product

Recombinant Coagulation Factor Concentrates

- Factor VIII

- Factor IX

- Others

Plasma-derived Coagulation Factor Concentrates

- Factor VIII

- Factor IX

- Others

Others

By Disease Indication

- Hemophilia A

- Hemophilia B

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Regional Analysis

North America

North America is expected to dominate the global market during the forecast period due to high diagnosis rates, advanced healthcare infrastructure, strong reimbursement systems, and presence of leading pharmaceutical companies.

Europe

Europe remains a significant market owing to strong government support for rare disease treatment and increasing adoption of recombinant therapies.

Asia Pacific

Asia Pacific is projected to witness the fastest growth due to rising healthcare expenditure, increasing awareness, and growing adoption of advanced hemophilia therapies in countries such as China and India.

Latin America

Latin America is expected to grow steadily due to improving healthcare systems and rising access to specialty treatments.

Middle East & Africa

The Middle East & Africa region is gradually emerging as a promising market with improving healthcare investments and growing awareness regarding rare bleeding disorders.

Why Buy This Report?

- Gain comprehensive insights into global hemophilia treatment drugs market trends

- Analyze key market drivers, restraints, and opportunities

- Understand competitive strategies adopted by major companies

- Evaluate market segmentation and regional growth prospects

- Access detailed analysis of emerging therapies and technologies

- Identify investment opportunities and future ROI potential

- Obtain strategic insights for business expansion and product development

- Understand evolving regulatory and reimbursement landscapes

- Benchmark leading companies and pipeline developments

- Support informed decision-making with accurate market forecasts

Frequently Asked Questions (FAQs)

1. What is the projected value of the global hemophilia treatment drugs market by 2031?

The global hemophilia treatment drugs market is projected to reach US$ 18.6 billion by the end of 2031.

2. What is driving growth in the hemophilia treatment drugs market?

Major growth drivers include increasing R&D activities, rising prevalence of hemophilia, growing demand for long-acting non-replacement therapies, and advancements in gene therapy technologies.

3. Which region dominates the global hemophilia treatment drugs market?

North America currently dominates the market due to strong healthcare infrastructure, higher diagnosis rates, and significant investments in hemophilia treatment programs.

4. Which product segment holds the largest market share?

Recombinant coagulation factor concentrates account for the largest market share owing to increasing adoption and ongoing innovation in recombinant therapies.

5. Who are the major players operating in the hemophilia treatment drugs market?

Key companies include Pfizer Inc., CSL Behring, Takeda Pharmaceutical Company Limited, Novo Nordisk A/S, Bayer AG, F. Hoffmann-La Roche Ltd., Octapharma AG, and Sanofi S.A.

Leave a Reply