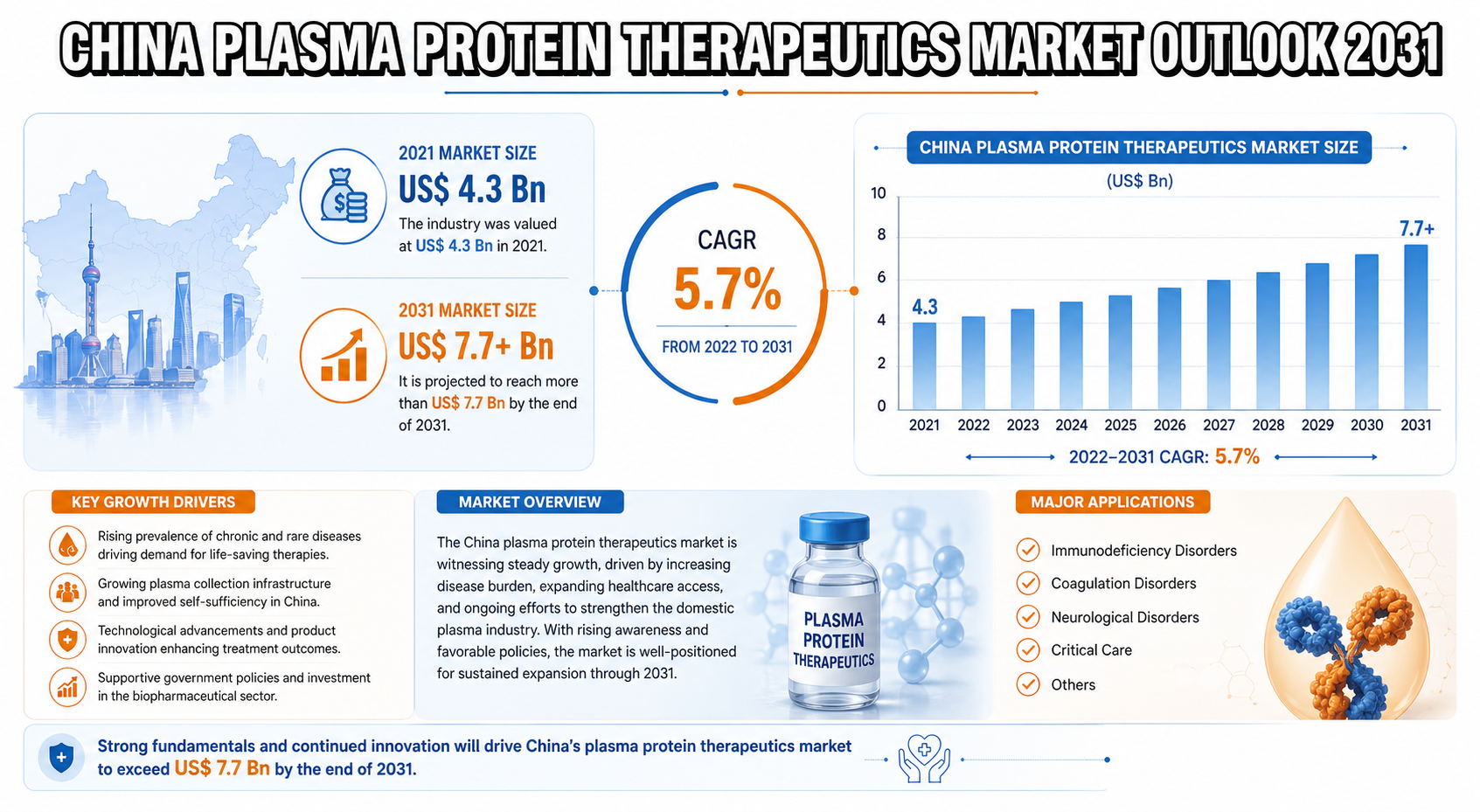

The China plasma protein therapeutics market was valued at US$ 4.3 billion in 2021 and is projected to exceed US$ 7.7 billion by 2031, growing at a compound annual growth rate (CAGR) of 5.7% from 2022 to 2031.

The market growth reflects rising demand for plasma-derived therapies used in treating chronic and rare diseases, alongside expanding healthcare infrastructure and increasing government support for advanced biologics in China.

Gain an understanding of key findings from our Report in this sample –

https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=85322

Market Overview

Plasma protein therapeutics are life-saving biologic products derived from human plasma and are widely used in the treatment of:

- Immune deficiencies

- Blood clotting disorders

- Neurological conditions

- Autoimmune diseases

Key plasma-derived products include immunoglobulins, albumins, coagulation factors, and C1-esterase inhibitors.

China’s market is undergoing rapid transformation due to:

- Rising burden of chronic diseases

- Expansion of plasma collection and fractionation capacity

- Increased healthcare spending

- Government focus on rare disease diagnosis and treatment

- Growing adoption of biologic and gene therapy solutions

The increasing elderly population and environmental risk factors further contribute to demand for plasma-based therapies.

Key Market Growth Drivers

1. Rising Prevalence of Chronic and Autoimmune Diseases

China is experiencing a sharp rise in conditions such as:

- Rheumatoid arthritis

- Systemic lupus erythematosus

- Multiple sclerosis

- Inflammatory bowel disease

- Hemophilia and coagulation disorders

These conditions significantly increase demand for immunoglobulin and coagulation factor therapies, driving market expansion.

2. Increasing Geriatric Population

China’s aging population is a major structural driver. By 2035, nearly 20% of the population is expected to be aged 65 and above, increasing susceptibility to immune deficiencies, neurological disorders, and hematological diseases.

3. Rising Healthcare Expenditure

China’s healthcare spending has grown significantly, rising from ~4% of GDP in 2000 to nearly 9% in 2020, enabling wider access to expensive biologic therapies.

4. Growth in Immunoglobulin Demand

Immunoglobulins dominate the market due to:

- Expanding treatment of immune deficiencies

- Rising autoimmune disease prevalence

- Strong reimbursement support

- Advancements in plasma fractionation technologies

5. Government Support for Rare Disease Treatment

China is actively investing in:

- Rare disease diagnosis programs

- Plasma collection infrastructure

- Domestic biologics manufacturing

This is accelerating supply-side expansion and improving treatment accessibility.

Analysis of Key Players – Key Player Strategies

The China plasma protein therapeutics market is moderately consolidated with strong participation from global and domestic biopharmaceutical companies.

Key Players:

- CSL Behring

- Grifols, S.A.

- Takeda Pharmaceutical Company Limited

- Octapharma AG

- Kedrion S.p.A.

- Biotest AG

- Shanghai RAAS

- Taibang Biological Group

- Biognosys AG

Key Strategies Adopted by Market Leaders

1. Expansion of Plasma Collection Networks

Companies are investing in plasma donation centers to secure raw material supply and reduce dependency risks.

2. Strategic Partnerships and Government Collaboration

Firms are partnering with healthcare authorities to enhance immunoglobulin availability and national self-sufficiency.

3. Product Innovation and R&D Investment

Focus is on:

- Safer immunoglobulin formulations

- Advanced fractionation technologies

- Plasma proteomics research

4. Localization of Manufacturing

International players are establishing production facilities in China to benefit from regulatory support and lower production costs.

5. Mergers, Acquisitions, and Licensing Deals

Companies are expanding portfolios through strategic acquisitions and long-term supply agreements.

Market Challenges & Opportunities

Challenges

- High cost of plasma-derived therapies

- Limited plasma donation rates relative to demand

- Strict regulatory requirements

- Complex manufacturing and safety processes

- Supply chain dependency on human plasma availability

Opportunities

- Expansion of domestic plasma collection infrastructure

- Growth in immunoglobulin and rare disease therapies

- Increasing adoption of gene therapy integration

- Rising demand in neurology and hematology applications

- Strong government focus on healthcare modernization

The market is expected to benefit significantly from China’s push toward biologics self-sufficiency.

Key Player Strategies

Leading companies are focusing on long-term structural expansion through:

- Capacity expansion in plasma fractionation facilities

- Strengthening immunoglobulin supply chains

- Investment in clinical research for rare diseases

- Strategic alliances with hospitals and government programs

- Enhancing distribution networks across Tier 1 and Tier 2 cities

Recent Developments

- In September 2022, Grifols signed a long-term agreement with Canadian Blood Services, Canada’s national blood authority, to increase the country’s self-sufficiency in immunoglobulin (Ig) medicines. Under the agreement, Grifols is expected to provide around 2.4 million grams of Ig annually.

- In March 2021, Biognosys announced its R&D roadmap for plasma proteomics as an unbiased, true discovery offering for large-scale applications.

Investment Landscape and ROI Outlook

The China plasma protein therapeutics market presents a high-value, high-barrier investment environment driven by essential healthcare demand and strong policy backing.

Investment Highlights

- Stable long-term demand due to chronic disease prevalence

- Strong government support for biologics and rare disease treatment

- Growing domestic manufacturing capabilities

- Increasing demand for immunoglobulins and coagulation factors

ROI Outlook

Investments in plasma fractionation facilities, immunoglobulin production, and localized manufacturing are expected to deliver strong and stable ROI, supported by:

- High product dependency in clinical care

- Limited substitution risk

- Expanding reimbursement coverage

- Growing patient base

The market offers particularly strong returns in immunoglobulin production and neurology-focused plasma therapies.

Market Segmentations

By Product Type

- Albumins

- Immunoglobulins

- Coagulation Factors

- C1-esterase Inhibitors

- Others

By Therapeutic Area

- Immunology

- Neurology

- Hematology

- Pulmonology

- Others

By Country

- China

Immunoglobulins dominate the product segment due to strong demand in immune deficiency and autoimmune disease treatment.

Immunology leads the therapeutic area segment owing to rising autoimmune disorder prevalence.

Why Buy This Report?

- Detailed 2022–2031 market forecast with CAGR analysis

- Comprehensive segmentation by product type and therapeutic area

- In-depth competitive landscape of global and Chinese players

- Analysis of regulatory environment and government healthcare policies

- Investment-focused insights with ROI potential evaluation

- Strategic overview of supply chain and plasma collection infrastructure

- Identification of high-growth therapeutic segments

FAQs

1. What is the size of the China plasma protein therapeutics market?

The market was valued at US$ 4.3 billion in 2021 and is projected to exceed US$ 7.7 billion by 2031.

2. What is the growth rate of the market?

The market is expected to grow at a CAGR of 5.7% from 2022 to 2031.

3. Which product type dominates the market?

Immunoglobulins hold the largest share due to rising autoimmune and immune deficiency disorders.

4. Which therapeutic area leads the market?

Immunology is the leading therapeutic area segment in China.

5. What are the key drivers of market growth?

Key drivers include rising chronic disease prevalence, aging population, increasing healthcare spending, and government support for rare disease treatment.

Leave a Reply