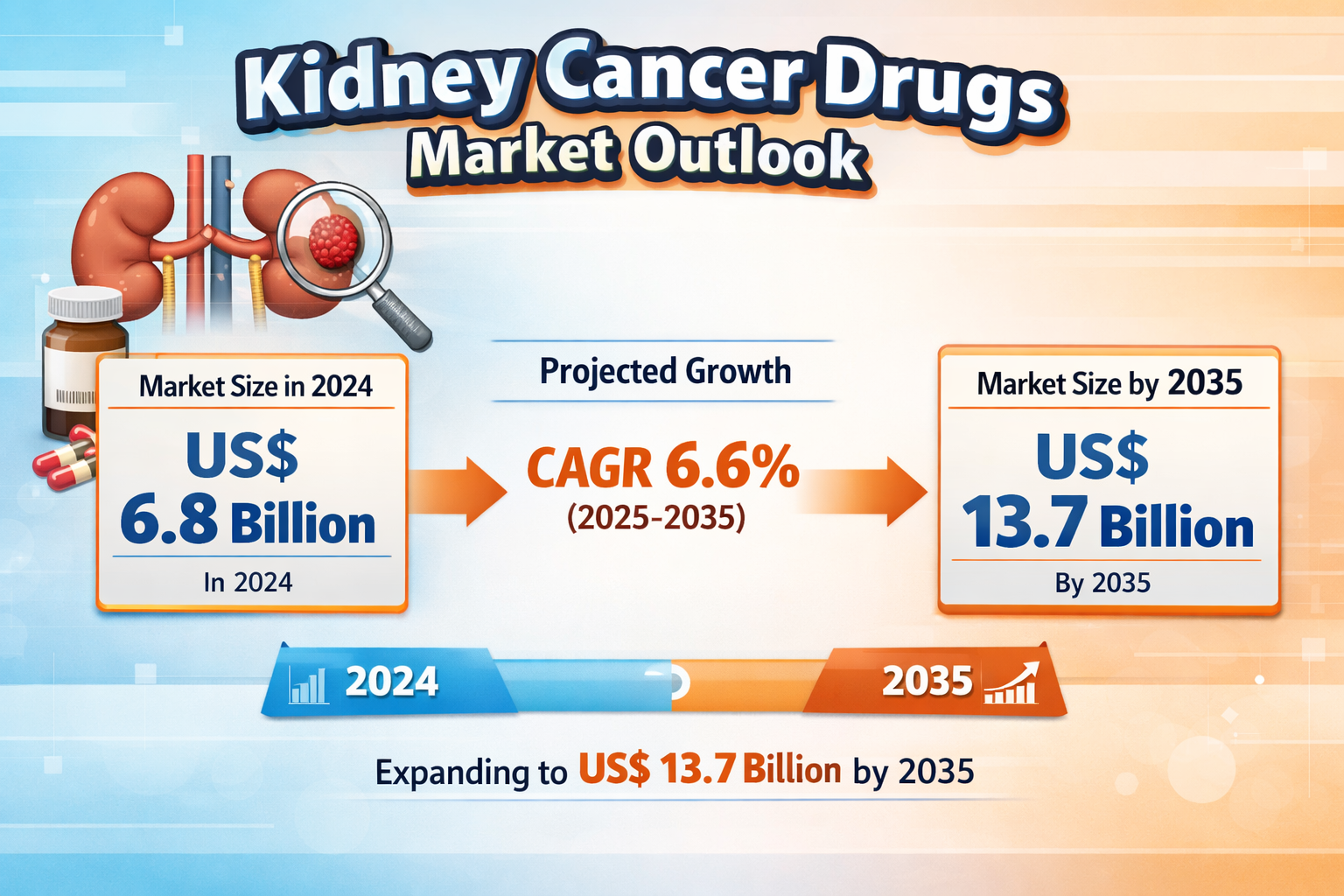

The global kidney cancer drugs market is witnessing steady and sustained growth, driven by advancements in oncology therapeutics and increasing disease prevalence. The market was valued at US$ 6.8 billion in 2024 and is projected to reach US$ 13.7 billion by 2035, expanding at a compound annual growth rate (CAGR) of 6.6% during the forecast period from 2025 to 2035.

This upward trajectory reflects the growing demand for effective, personalized treatment options and the continuous innovation in drug development, particularly in targeted therapy and immunotherapy. The expansion is also supported by rising healthcare expenditure and improved access to advanced medical treatments globally.

Explore core findings and critical insights from our Report in this sample –

https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=537

Market Overview

The kidney cancer drugs market encompasses pharmaceutical treatments designed to combat various forms of kidney cancer, including renal cell carcinoma (RCC), renal urothelial carcinoma, and transitional cell carcinoma. Among these, renal cell carcinoma (RCC) dominates the market, accounting for 81.4% of the total share in 2024, owing to its high incidence rate and extensive therapeutic research focus.

Over the years, the market has transitioned significantly from conventional chemotherapy to more advanced treatment modalities such as targeted therapies and immuno-oncology drugs. These newer approaches offer improved survival rates, reduced side effects, and enhanced quality of life for patients.

The increasing adoption of biomarker-based therapies and combination treatment regimens is reshaping the competitive landscape. Pharmaceutical companies are investing heavily in research and development to introduce innovative drugs and expand their oncology portfolios.

Geographically, North America leads the global market with a 37.5% revenue share in 2024, supported by robust healthcare infrastructure, high disease awareness, and strong presence of leading pharmaceutical companies.

Key Market Growth Drivers

One of the primary drivers of the kidney cancer drugs market is the rising incidence of kidney cancer worldwide. Factors such as aging populations, increasing obesity rates, smoking, alcohol consumption, and chronic kidney diseases are contributing to the growing number of diagnosed cases. Improved diagnostic technologies have also enabled earlier and more accurate detection, further increasing treatment demand.

Another significant growth factor is the increase in global healthcare expenditure. Governments and private organizations are investing more in cancer research, healthcare infrastructure, and access to advanced therapies. This has facilitated the adoption of innovative drugs, particularly in emerging economies where healthcare access is rapidly improving.

Additionally, the shift toward targeted therapy and immunotherapy is accelerating market growth. These therapies, including immune checkpoint inhibitors and angiogenesis inhibitors, have demonstrated superior clinical outcomes compared to traditional chemotherapy. Combination therapies are also gaining traction, offering enhanced efficacy and improved patient survival rates.

The expansion of precision medicine and biomarker-guided treatment approaches is further fueling demand, enabling more personalized and effective treatment strategies.

Analysis of Key Players – Key Player Strategies

The global kidney cancer drugs market is highly competitive, with several leading pharmaceutical companies actively engaged in innovation, strategic collaborations, and market expansion.

Major players such as AstraZeneca, Bayer AG, Bristol-Myers Squibb Company, Eisai Co., Ltd., F. Hoffmann-La Roche AG, GSK plc., Merck & Co., Inc., Novartis Pharmaceuticals Corporation, Pfizer Inc., Johnson & Johnson, and Exelixis, Inc. are focusing on strengthening their oncology pipelines.

Key strategies adopted by these players include:

- Intensive Research & Development (R&D): Companies are investing heavily in developing next-generation therapies, including HIF-2α inhibitors, monoclonal antibodies, and combination regimens.

- Strategic Collaborations and Partnerships: Collaborations with biotech firms and research institutions are helping accelerate drug development and clinical trials.

- Expansion of Indications: Existing drugs are being tested and approved for additional treatment lines and cancer stages, increasing their market potential.

- Geographic Expansion: Companies are expanding their footprint in emerging markets such as Asia-Pacific and Latin America to tap into growing patient populations.

- Focus on Combination Therapies: Combining immunotherapy with targeted therapy is becoming a key strategy to enhance treatment efficacy.

Market Challenges & Opportunities

Despite its promising growth, the kidney cancer drugs market faces several challenges. One of the primary obstacles is the high cost of advanced therapies, which can limit patient access, especially in low- and middle-income countries. Variability in reimbursement policies across regions further complicates market penetration.

Another challenge is the complex regulatory landscape, which can delay drug approvals and increase development costs. Additionally, competition among pharmaceutical companies is intensifying, leading to pricing pressures and reduced profit margins.

However, these challenges are accompanied by significant opportunities. The growing focus on personalized medicine and biomarker-driven therapies presents a major avenue for innovation. Advances in genomics and molecular diagnostics are enabling more precise treatment approaches.

Emerging markets offer substantial growth potential due to improving healthcare infrastructure and increasing awareness of cancer treatment options. Furthermore, the development of novel drug classes and combination therapies continues to open new revenue streams for market players.

Key Player Strategies

Leading companies are increasingly focusing on:

- Pipeline diversification to reduce dependency on single drug categories

- Adoption of advanced technologies such as AI in drug discovery

- Strengthening distribution networks to enhance market reach

- Mergers and acquisitions to consolidate market position

- Patient-centric approaches, including affordability programs and improved access initiatives

These strategies are helping companies maintain competitive advantage and drive long-term growth.

Recent Developments

In October 2025, Merck & Co., Inc. introduced Belzutifan, as it achieved its main goal in two Phase III studies in advanced renal cell carcinoma (RCC) – an adjuvant setting trial and a relapsed disease after prior therapies trial. A HIF-2a inhibitor that could be used in different scenarios of kidney cancer, the company indicated, as the results might be first broadened to the next stages of less-advanced disease.

In February 2025, Zircaix BLA by Telix Pharmaceuticals was accepted by the FDA and hence Priority Review was granted by the FDA. Zircaix is a PET imaging agent targeting clear cell renal cell carcinoma (ccRCC). If the FDA approves the product, it will be the first radiodiagnostic imaging agent commercially available for ccRCC.

In April 2024, Junshi Biosciences announced that the China National Medical Products Administration (NMPA) approved the supplemental new-drug application (sNDA) for the combined use of Toripalimab (JS001) and Axitinib as a first-line treatment for a patient with a medium- to high-risk unresectable or metastatic renal cell carcinoma (RCC).

In June 2024, Bristol Myers Squibb has revealed phase 3 data from its CheckMate-67T trial showing that a subcutaneous (under-the-skin) formulation of Opdivo (nivolumab) achieves drug exposure and efficacy comparable to the standard intravenous version in patients with advanced or metastatic renal-cell carcinoma.

Investment Landscape and ROI Outlook

The kidney cancer drugs market presents a highly attractive investment landscape, characterized by consistent growth and strong demand for innovative therapies. Venture capital investments, strategic partnerships, and increased funding for oncology research are driving the development of new treatment options.

Return on investment (ROI) is expected to remain favorable due to the high value of oncology drugs, long treatment durations, and expanding patient populations. Companies that invest in breakthrough therapies and precision medicine are likely to achieve significant competitive advantages.

Moreover, government support for cancer research and favorable regulatory frameworks in key markets are encouraging investments. The expansion of clinical trials and the introduction of novel drug classes further enhance the market’s long-term profitability potential.

Market Segmentations

The kidney cancer drugs market is segmented based on cancer type, therapy, drug class, route of administration, distribution channel, and region.

By Cancer Type:

- Renal Cell Carcinoma (RCC)

- Renal Urothelial Carcinoma

- Transitional Cell Cancer

- Others

By Therapy:

- Targeted Therapy

- Immunotherapy

- Chemotherapy

- Others

By Drug Class:

- Angiogenesis Inhibitors

- Monoclonal Antibodies

- mTOR Inhibitors

- Cytokine Immunotherapy (IL-2)

- Others

By Route of Administration:

- Oral

- Intravenous

- Others

By Distribution Channel:

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Region:

- North America (U.S., Canada)

- Europe (Germany, U.K., France, Italy, Spain, The Netherlands)

- Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN)

- Latin America (Brazil, Mexico, Argentina)

- Middle East & Africa (GCC Countries, South Africa)

North America remains the dominant region, while Asia Pacific is expected to witness the fastest growth due to improving healthcare infrastructure and rising patient awareness.

Why Buy This Report?

- Gain comprehensive insights into market size, growth trends, and future projections

- Understand key drivers, challenges, and emerging opportunities

- Analyze competitive landscape and key player strategies

- Access detailed segmentation and regional analysis

- Stay updated with recent developments and innovations in the market

- Identify investment opportunities and strategic growth areas

- Support business decisions with reliable and data-driven insights

FAQs

1. What is the current size of the kidney cancer drugs market?

The market was valued at US$ 6.8 billion in 2024 and is expected to reach US$ 13.7 billion by 2035.

2. What is driving the growth of this market?

Key drivers include rising incidence of kidney cancer, increasing healthcare expenditure, and advancements in targeted therapies and immunotherapy.

3. Which segment dominates the market?

Renal Cell Carcinoma (RCC) dominates the market, accounting for over 81% share.

4. Which region leads the global market?

North America leads the market with a 37.5% share, driven by advanced healthcare infrastructure and strong R&D activities.

5. Who are the major players in the market?

Leading companies include AstraZeneca, Bayer AG, Bristol-Myers Squibb, Roche, Merck & Co., Pfizer, Novartis, and others.

Leave a Reply