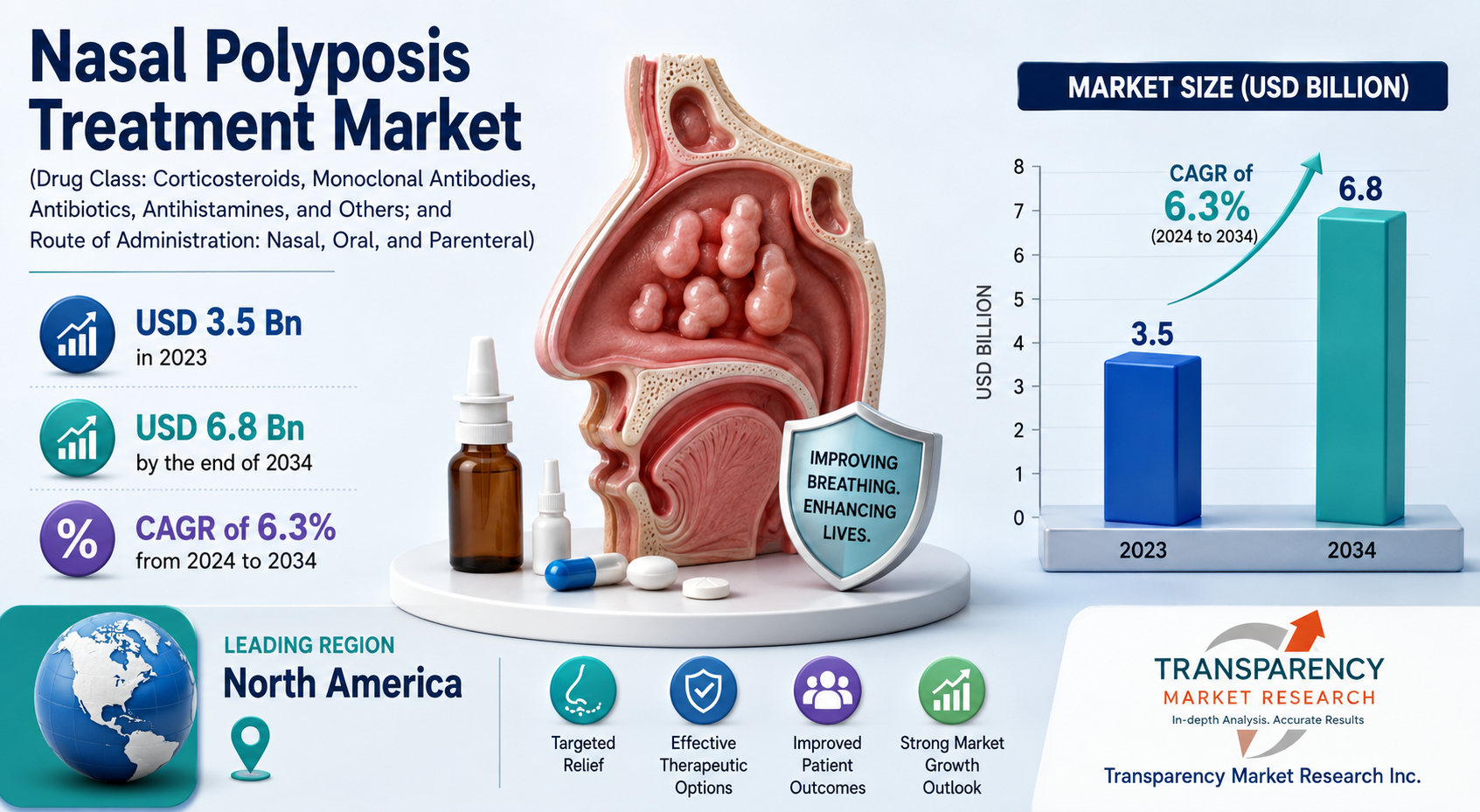

The global Nasal Polyposis Treatment market was valued at USD 3.5 billion in 2023 and is projected to reach USD 6.8 billion by the end of 2034. The market is expected to expand at a CAGR of 6.3% from 2024 to 2034, driven by the rising prevalence of chronic rhinosinusitis with nasal polyps, increasing awareness regarding advanced treatment options, and growing adoption of biologics and minimally invasive therapies.

👉 Get sample market research report copy today@ https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=53529

Market Overview

The global nasal polyposis treatment market is slated to grow exponentially due to the continuous launch of new products by the key players, followed by an increase in the number of retail pharmacies providing these drugs. Nasal polyposis, also called nasal polyps, is pink or yellowish in color and hangs down, resembling grapes.

The companies operating in the nasal polyposis treatment market are delving deeper into the existing measures of treatment for nasal polyposis in order to provide a higher level of relief to the patients, subsiding the side-effects such as cough, cold, swelling of eyes, and the like. They are also exploring the probability of devising new drugs with the mitigation of side effects mentioned above.

Analysts’ Viewpoint

Measures of treatment available include nasal steroids, oral steroids, biologic medicines (that are subject to maximum research), and others such as aspirin desensitization to help those suffering from nasal polyps and allergic to aspirin. This desensitization may be succeeded by daily aspirin therapy.

However, there are certain side effects of the drugs used to remove nasal polyps. They include thick nasal discharge, severe facial pain, cough, chills, sore throat, fever, and various other signs of infection, such as a whistling sound from hives, nose, itching, rashes, swelling of the face, lips, tongue, lower legs, ankles, feet, and eyes.

Analysis of Key Players

The global competitive landscape features a distinct divide between massive multinational pharmaceutical conglomerates managing high-margin specialty biologics and established medical technology firms engineering local drug-eluting structural implants.

Leading companies operating in this market include:

- Sanofi (Partnered with Regeneron Pharmaceuticals, Inc.)

- GSK plc

- AstraZeneca plc

- Amgen Inc.

- Novartis AG

- Genentech, Inc. (Roche Group)

- Intersect ENT, Inc. (Acquired by Medtronic)

- OptiNose, Inc.

- Pfizer Inc.

- Merck KGaA

- Eli Lilly and Company

The industry is moderately consolidated, with major entities investing heavily in expanded indication approvals. The competitive standard relies on securing long-term real-world evidence (RWE) demonstrating that a specific molecule not only shrinks physical polyp volume but also significantly restores the patient’s sense of smell (anosmia resolution) and reduces the long-term economic burden of repeat surgical procedures.

Recent Developments (2025-2026)

- Late 2025: Amgen and AstraZeneca secured regulatory clearance expanding the utility of Tezspire (tezepelumab-ekko) as an add-on maintenance treatment for adults and adolescents with severe chronic rhinosinusitis with nasal polyps, targeting upstream thymic stromal lymphopoietin (TSLP) pathways.

- Mid 2025: GSK advanced its long-acting interleukin-5 inhibitor pipeline (depemokimab), with key global regulatory filings moving into fast-track review matrix arrays aimed at reducing dosing frequencies to a convenient half-yearly subcutaneous injection window.

- Early 2025: Digital health integrations expanded across specialty pharmacies, deploying smart-phone linked endoscope attachments and AI symptom trackers to allow patients to record polyp regression patterns remotely and share them directly with their ENT clinics.

👉 Discuss Implications for Your Industry Request Sample Research Report PDF@ https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=53529

Key Developments & Trends

- The Biologics Proliferation: Monoclonal antibodies represent the fastest-expanding treatment sub-segment, growing at an 8.2% CAGR as clinicians prioritize long-term chemical disease modification over temporary surgical removal.

- Exhalation Delivery Systems (EDS): Delivery technologies like XHANCE are capturing substantial market volume, growing at over 8.3% annually due to their ability to leverage a patient’s own exhaled breath to guide anti-inflammatory medication deep into covered sinus channels.

- Bio-Resorbable Stent Advancements: High utilization of in-office, steroid-eluting sinus implants that physically prop open sinus passages post-surgery while slowly dissolving to release micro-doses of mometasone furoate directly into the mucosal wall.

- The Telehealth and E-Prescription Shift: Online pharmacy distribution networks for maintenance sinus therapies are expanding at a 9.0% CAGR, supported by digital ENT triage consultations and direct-to-home specialty cold-chain logistics.

Challenges

- High Economic and Therapy Cost Barriers: Annual specialty biological regimens often exceed USD 30,000 per patient, triggering strict pre-authorization insurance hoops and limiting market penetration within emerging economic zones.

- Steroid-Induced Local Complications: Prolonged reliance on heavy high-dose corticosteroid sprays carries risks of mucosal atrophy, epistaxis (nasal bleeding), and septal perforations, leading to patient drop-outs.

- Strict Plant and Implant Compliance Mandates: Navigating complex international approval frameworks for medical-device/drug hybrid implants requires lengthy multi-center trial evaluations, slowing early cross-border distribution.

- Surgical Access Inertia: In several developing healthcare systems, localized clinical pathways remain heavily biased toward affordable, one-time manual polypectomies over continuous, long-term biological care profiles.

Opportunities

- Biomarker-Driven Precision Companion Diagnostics: Creating rapid, in-office nasal secretion test kits to identify specific tissue eosinophilia or IgE markers, allowing general practitioners to instantly match patients to the correct biologic.

- Long-Acting Next-Gen Small Molecules: Developing highly localized, durable JAK (Janus kinase) inhibitors optimized for topical sinus delivery, offering biologic-like efficacy without the need for systemic injections.

- Strategic Penetration into Emerging APAC Hubs: Customizing access programs and scaling tier-2 manufacturing hubs across China and India, which are currently recording the world’s fastest regional growth rates (7.1% to 8.0%).

- Combination Barrier and Elution Arrays: Engineering hybrid nasal packing materials that combine immediate post-operative mechanical hemostasis (stopping blood flow) with micro-encapsulated, timed-release anti-polyp agents.

Market Segmentation

➤ By Drug Class & Modality

- Corticosteroids (Intranasal and Oral) (Leading Segment – Controlling roughly 41% to 45% of total market value due to universal positioning as the mandatory first-line, affordable therapeutic standard).

- Biologic Therapies (Monoclonal Antibodies) (Fastest Growing Segment – Expanding rapidly as clinical evidence confirms superior long-term control over severe, recurring polyposis).

- Antibiotics, Antihistamines, & Leukotriene Modifiers (Stable Volume Segment – Frequently utilized as auxiliary therapies to manage secondary bacterial sinus infections and underlying allergic triggers).

- Surgical Interventions (FESS/Polypectomy) (Structural Segment – Remains an important mechanical option for immediate airway clearance in severe, completely obstructive cases).

➤ By Route of Administration

- Intranasal (Sprays, Rinses, and EDS) (Dominant Route – Representing over 45% to 48% of the operational footprint, preferred for localized delivery, minimized systemic side effects, and ease of self-administration).

- Subcutaneous Injection (Fastest Growing Route – Directly tied to the expanding administration of self-injectable biologic pens for long-term maintenance).

- Oral (Conventional Route – Limited to short-term, acute systemic rescue bursts to shrink massive tissue obstructions rapidly).

➤ By End User & Distribution

- Hospitals & Ambulatory Surgical Centers (Leading End User – Capturing over 50% share, driven by complex endoscopic sinus surgery procedures and inpatient diagnostics).

- ENT and Otolaryngology Specialist Clinics (Fastest Growing Prescriber Node – Gaining rapid ground via specialized diagnostic nasal endoscopy and targeted biologic prescribing infrastructure).

- Hospital & Retail Pharmacies (Primary Distribution Channels – Holding the majority of traditional volume fulfillment).

- Online Pharmacies (Emerging Channel – Accelerating at a 9.08% CAGR on the back of automated specialty drug renewal protocols).

➤ By Geography

- North America (Largest Revenue Share – Commanding roughly 42% of global market value, supported by advanced specialty pharmacy networks, robust private reimbursement framework for biologics, and high clinical awareness).

- Europe (Highly Mature Market – Characterized by structured, guideline-driven clinical pathways and extensive state-backed institutional reimbursement programs for severe CRSwNP).

- Asia-Pacific (Fastest Growing Regional Market – Expanding at an accelerated 7.1% to 8.0% CAGR, driven by large patient populations, rapid expansion of urban ENT infrastructure, and increasing market penetration by international pharmaceutical developers in China, Japan, and India).

👉 To buy this comprehensive market research report, click here to inquire@ https://www.transparencymarketresearch.com/checkout.php?rep_id=53529<ype=S

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Abhishek Budholiya

Transparency Market Research Inc.

State Tower, 90 State Street, Suite 700,

Albany NY – 12207, United States

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

Leave a Reply