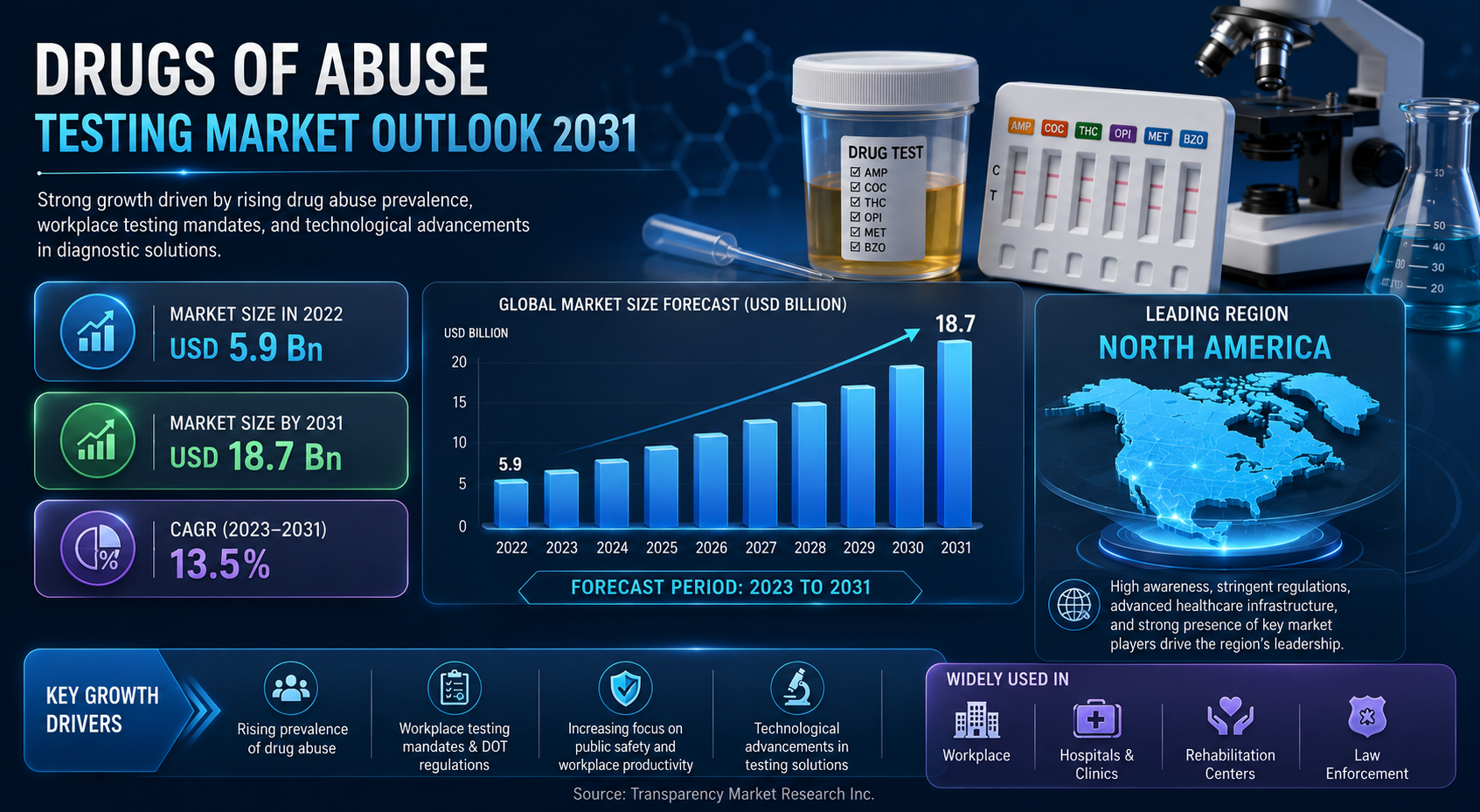

The global Drugs of Abuse Testing market was valued at USD 5.9 billion in 2022 and is projected to reach USD 18.7 billion by 2031, expanding at a CAGR of 13.5% from 2023 to 2031. Market growth is driven by increasing drug screening programs, rising substance abuse cases, and growing demand for workplace and forensic testing solutions.

Dive Deeper into Data: Get Your In-Depth Sample Now! https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=85980

Analyst Viewpoint

Rise in cases of drug abuse is fueling the drugs of abuse testing market size. Urine testing is the most common test as it is non-invasive, quick, and able to qualitatively detect a wide range of drugs.

Approval and launch of new tests is driving the drugs of abuse testing market trajectory. LC-tandem-MS are becoming a new gold standard for confirmatory substance abuse screening with selected ion monitoring (SIM) for immunoassay confirmation, targeted screening, and quantification.

Major players operating in the drugs of abuse testing market landscape are reducing product costs to provide greater access to high-quality drug abuse tests for people living in the least developed countries, where the need is most urgent.

Market Introduction

Drugs of abuse testing detects the presence or absence of commonly abused medicines. Drugs that are abused can be classified into natural drugs, semi-synthetic drugs, and synthetic drugs.

Natural drugs are sourced from one of the following three plants – opium poppy (Papaver somniferous), cannabis, and coca. Alcohol, cocaine, opioids, inhalants, marijuana, 3, 4-methylenedioxy-N-methamphetamine (MDMA), methamphetamine, nicotine, psychedelics, dissociative drugs, and GHB & Rohypnol are the most common drugs of abuse.

Drugs of abuse testing looks for the presence of small molecules (metabolites) released during the breakdown of any of these ingested medicines. This testing is widely used in clinical and forensic settings. Urine is the preferred type of specimen for drugs of abuse testing.

Macro Growth Drivers

- Mandatory Workplace Safety & Transport Regulations

Safety-sensitive industries—such as aviation, commercial logistics, construction, and manufacturing—are legally bound to maintain zero-tolerance policies. Strict government bodies, like the U.S. Department of Transportation (DOT), continually mandate random and pre-employment screening.

- The Shift to Non-Invasive Point-of-Care (POC) Testing

While urine testing remains the historical baseline, there is a massive shift toward oral fluid (saliva) and breath testing. Oral fluid tests are expanding rapidly because they drastically lower privacy objections, eliminate the risk of sample tampering (such as synthetic urine substitution), and provide a shorter, highly accurate window of detection relevant to immediate impairment.

- The Threat of Synthetic & Designer Drugs

Traditional testing panels are frequently failing to catch rapidly shifting illicit chemical structures. The market is adjusting by scaling up multi-panel testing kits that can detect highly specialized synthetic opioids (like fentanyl and norfentanyl), designer stimulants, and psychostimulants.

- Integration of Digital & Cloud Reporting

Modern corporate and forensic users are moving away from manual paperwork. Rapid screening devices now utilize digital readers, mobile data capture, and cloud-based compliance tracking to automatically transmit electronic custody-and-control forms directly to human resource departments or legal entities.

Key Market Segmentation

By Product & Service

- Consumables (Largest Segment): Holds roughly 38% of the market share. This includes rapid testing cassettes, multi-panel cups, reagents, and collection strips that drive continuous, recurring revenue.

- Laboratory Services: Expected to yield the fastest growth. Complicated or legally contested initial rapid screens must be confirmed using highly specialized laboratory instruments like Mass Spectrometry.

By Sample Type

| Sample Type | Market Nuance & Adoption Rate |

| Urine | Dominates the market (over 41% share) due to deeply entrenched legal protocols and extended detection windows. |

| Oral Fluid (Saliva) | Growing at the fastest rate (~8.7% CAGR), heavily favored for roadside testing and corporate onboarding. |

| Hair & Breath | Hair testing is highly utilized for executive-level or child custody screening due to its 90-day detection window. Breath analyzers remain dominant for immediate alcohol screening. |

By Technology

- Immunoassay / Lateral Flow Assays: Represents the front line of screening. Immunoassay technologies account for roughly 45% of the revenue due to their low cost and quick results. Lateral flow formats utilizing gold nanoparticles are advancing rapidly to approach laboratory-grade sensitivity levels.

- Chromatography & Spectroscopy: The definitive gold standard (LC-MS/MS, GC-MS) used exclusively in clinical and forensic laboratories for absolute confirmation of a positive screen.

Regional Landscape

- North America: Commands the largest share of the market (~38-39%). This is heavily driven by the ongoing opioid epidemic in the United States, strict federal testing laws, and high corporate adoption of random workplace drug screening.

- Europe: Accounts for roughly 27% of the market, with Germany and the UK leading. Demand is centered heavily around criminal justice systems, roadside sobriety screening, and European workplace safety laws.

- Asia-Pacific: Highlighted as the fastest-growing region (projected ~9.1% CAGR). Rapid urbanization, expansion of manufacturing sectors with strict labor laws, and tightening forensic enforcement in countries like China and India are pulling massive testing volumes.

Dominant Industry Competitors

The global competitive environment is highly consolidated around a few prominent medical device and diagnostic titans:

- Abbott Laboratories (Leading the market with significant share via its Alere acquisition)

- Thermo Fisher Scientific Inc. (Dominates in high-end laboratory analyzers and reagents)

- Danaher Corporation (Beckman Coulter diagnostics arm)

- Siemens Healthineers (Automated clinical chemistry and immunoassay lines)

- F. Hoffmann-La Roche Ltd. (Global diagnostics leader)

- Quest Diagnostics & LabCorp (The definitive leaders in outsourced commercial laboratory services)

- Drägerwerk AG & Co. KGaA (Niche leaders in roadside breath and oral fluid testing systems)

Buy this Premium Research Report: https://www.transparencymarketresearch.com/checkout.php?rep_id=85980<ype=S

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Abhishek Budholiya

Transparency Market Research Inc.

State Tower, 90 State Street, Suite 700,

Albany NY – 12207, United States

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

Leave a Reply