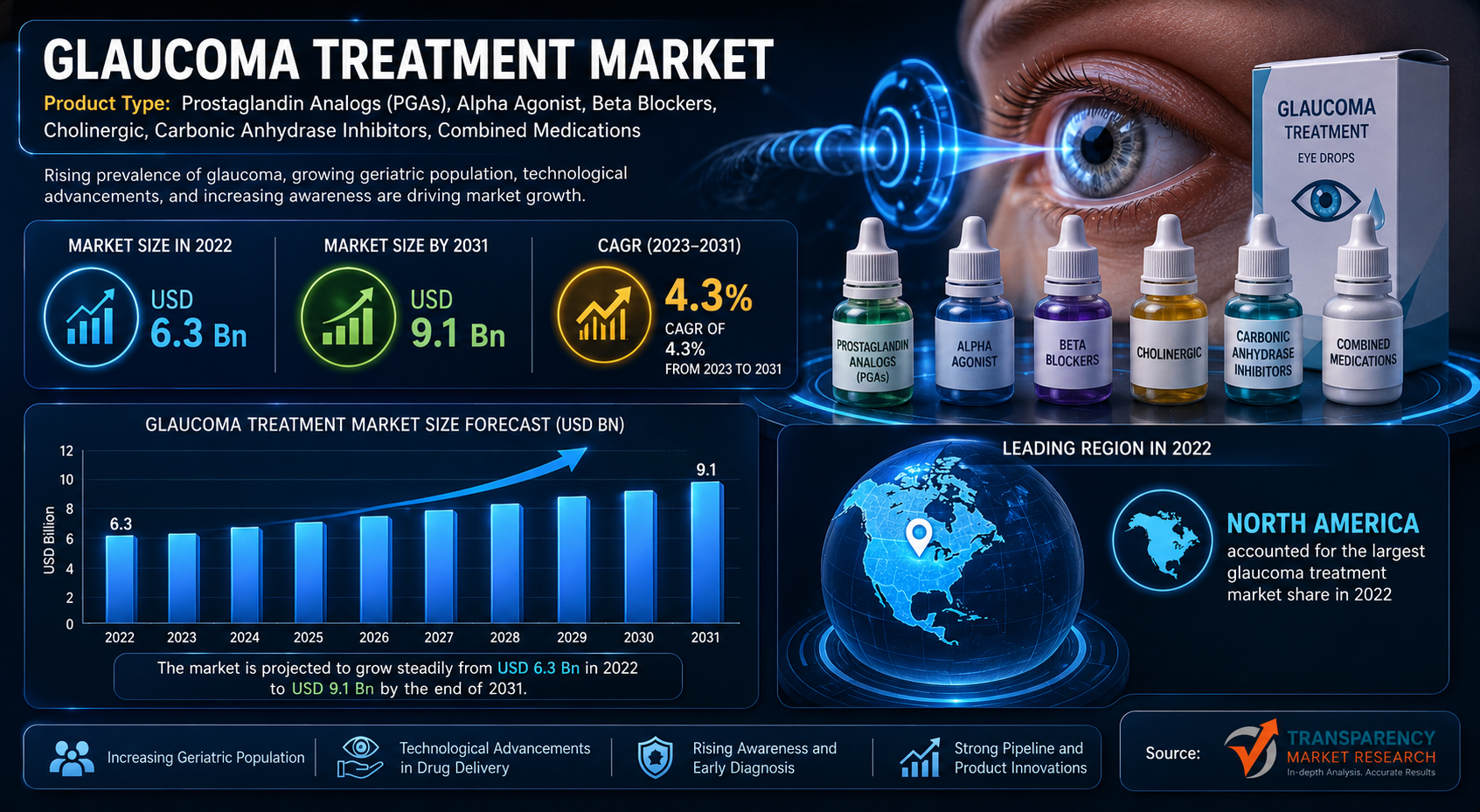

The global glaucoma treatment market was valued at USD 6.3 billion in 2022 and is projected to reach USD 9.1 billion by the end of 2031. The market is expected to grow at a CAGR of 4.3% from 2023 to 2031, driven by the rising prevalence of glaucoma, the increasing aging population, and the growing demand for advanced treatment options and early diagnosis.

👉 Get sample market research report copy today@ https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=16451

Market Overview

Glaucoma is the degeneration of retinal ganglion cells and retinal nerve fiber layers, which may result in an alteration in optical nerve head. Glaucoma is among the leading causes of irreversible blindness across the globe. Causes could include excessive smoking, vasospasm, age and frailty, myopia, systemic hypertension and hypotension, migraine, obstructive sleep apnea syndrome, increased IOP, and usage of steroids.

Latest innovations in glaucoma eye treatment, such as selective laser trabeculoplasty (SLT), medical imaging, optical coherence tomography (OCT), microinvasive glaucoma surgery (MIGS), visual fields, and progression analysis software, are helping in the early diagnosis. This is expected to help in the cure of glaucoma through over-the-counter fixed-combination dosages.

Analysts’ Viewpoint

Vision impairment or blindness is a serious health issue across the globe. The third-most common cause of blindness is glaucoma. If detected early, the progression of glaucoma can be stabilized or prevented through medical and surgical therapy. Rise in awareness and screening campaigns about glaucoma and the efficacy of fixed-dose combination products, which can help prevent the need for complex eye surgeries in the near future, is likely to boost the glaucoma treatment market growth in the next few years.

Leading pharmaceutical players are investing significantly in the development of innovative technologies for early glaucoma detection and treatment owing to the large incidence of this disease. Furthermore, rise in approvals for intraocular pressure (IOP) lowering drugs is expected to create lucrative glaucoma treatment market opportunities for several manufacturers in the next few years.

Analysis of Key Players

The competitive landscape is characterized by “Medium Concentration,” where a few dominant pharmaceutical and medical device giants aggressively invest capital into bio-erodible drug delivery systems and next-generation surgical stents.

Leading companies operating in the global glaucoma treatment market include:

- Alcon, Inc. (Global Market Leader in surgical devices and automated laser systems)

- Allergan (An AbbVie Company – Leader in sustained-release therapeutics)

- Bausch + Lomb Corporation

- Santen Pharmaceutical Co., Ltd.

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- Glaukos Corporation (Pioneer in MIGS implants)

- Aerie Pharmaceuticals (A subsidiary of Alcon)

- Nicox S.A.

Recent strategic moves show these players pivoting toward “Intelligent Interventions,” utilizing micro-stents and drug-eluting rings to establish predictable, long-term intraocular fluid drainage in the “Interventional Ophthalmology” segment.

Recent Developments (2025–2026)

- April 2026: Market intelligence highlighted that the Glaucoma Surgery Devices segment alone witnessed a massive valuation surge, driven by the rapid clinical integration of next-generation microcatheters and specialized diamond knives in ambulatory surgical centers.

- February 2025: Alcon launched the Voyager DSLT in the U.S., introducing an automated, gonio-lens-free Direct Selective Laser Trabeculoplasty device designed to streamline first-line therapy for ocular hypertension.

- Late 2025: Nicox completed its definitive Phase 3 Denali trial for NCX 470, an advanced nitric oxide-donating prostaglandin analog eye drop targeting open-angle glaucoma, preparing for formal FDA submission in early 2026.

- June 2025: Qlaris Bio advanced clinical development on a novel preservative-free fixed-dose combination pairing QLS-111 with latanoprost, aiming to reduce toxic ocular surface build-up for long-term users.

👉 Discuss Implications for Your Industry Request Sample Research Report PDF@ https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=16451

Key Developments & Trends

- Sustained-Release Drug Delivery: The shift from daily self-administered eye drops to physician-inserted, bio-erodible implants that slowly release medication over several months.

- Preservative-Free Formulations: Vital modifications in chemical chemistry to eliminate benzalkonium chloride (BAK), drastically reducing ocular irritation and dry-eye side effects.

- MIGS Expansion: Rapid proliferation of micro-stents that bypass blocked trabecular meshwork with minimal tissue trauma, altering early surgical paradigms.

- Dual-Mechanism Combinations: Fixed-dose single-drop therapies targeting both the trabecular and uveoscleral outflow pathways to maximize IOP reduction.

- Neuroprotection Pathways: Developing therapies like BDNF and ROCK inhibitors aimed at protecting the optic nerve directly, independent of pressure levels.

Challenges

- Asymptomatic Patient Non-Adherence: Chronic disease characteristics result in over 50% of patients discontinuing or incorrectly applying daily drop treatments due to a lack of immediate early symptoms.

- High Costs of Advanced Interventions: Premium micro-implants and novel drug classes face high accessibility barriers in low- and middle-income nations.

- Reimbursement Disparities: Inconsistent global insurance coverage for newly approved premium MIGS and long-acting therapeutics limits immediate market penetration.

- Stringent Regulatory Frameworks: Lengthy, multi-year clinical trials required to prove long-term safety and efficacy of intraocular devices.

Opportunities

- AI-Driven Early Diagnostics: Utilizing machine learning and cloud-based fundus cameras to detect early optic nerve changes before irreversible vision loss occurs.

- First-Line Laser Systems: Exploiting the clinical shift toward automated SLT systems to establish early, medication-free pressure control.

- Emerging Healthcare Infrastructure: Skyrocketing market potential in developing nations through scaled diagnostic screening programs and affordable generic combination treatments.

- Outpatient Care Migration: Gaining market share by optimizing therapeutic designs for quick, in-office or ambulatory surgical clinic procedures.

Market Segmentation

➤ By Disease Type

- Open-Angle Glaucoma (Highest Share ~71%, driven by higher prevalence and gradual clinical onset)

- Angle-Closure Glaucoma (Rapid progression potential, requiring swift emergency surgical or laser treatment)

- Secondary Glaucoma (Fastest Growing CAGR due to rising post-trauma, steroid-induced, and uveitic conditions)

➤ By Drug Class / Treatment

- Prostaglandin Analogs (Traditional Leader ~44% share, maximizing uveoscleral outflow)

- Beta Blockers & Alpha Agonists (Widely used core therapies to reduce aqueous humor production)

- Fixed-Dose Combinations & ROCK Inhibitors (Highest growth trajectory within therapeutics)

- Surgical & Laser Devices (MIGS, traditional trabeculectomy, and automated laser systems)

➤ By Distribution Channel

- Hospital Pharmacies (Leading Segment ~48.3% market share, due to centralized access to specialized ophthalmologists)

- Retail Pharmacies & Ophthalmic Clinics

- Online Pharmacies (Experiencing high growth via convenient home-delivery models for chronic medication refills)

Conclusion

The glaucoma treatment industry is no longer just about “lowering pressure via daily drops”; it is integrating deeply into the broader biopharma, advanced medical device, and digital data diagnostic ecosystems. Through 2035, the market will be defined by chemical stability, patient compliance mitigation, and micro-invasive surgical agility. As health networks pivot toward early intervention and long-acting, localized drug delivery, the companies capable of providing zero-toxicity, reliable, and neuroprotective therapeutic solutions will dictate the next generation of global ophthalmic care.

👉 To buy this comprehensive market research report, click here to inquire@ https://www.transparencymarketresearch.com/checkout.php?rep_id=16451<ype=S

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Abhishek Budholiya

Transparency Market Research Inc.

State Tower, 90 State Street, Suite 700,

Albany NY – 12207, United States

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

Sales Inquiries: sales@transparencymarketresearch.com

Media Inquiries: media@transparencymarketresearch.com

Leave a Reply